In the world of mergers and acquisitions, industry giants come together to create new opportunities and redefine the corporate landscape. It’s where fortunes are made and strategic alliances are forged.

However, despite your best efforts, the success of M&A is only partially within your control, as many external factors, including the political and economic climate, can influence the outcome.

We’ve created a concise overview of M&A activity in 2023, 2024 forecasts, and recent deals in M&A to give you valuable insights into various industries and potential investment or partnership opportunities.

For your convenience, we split this sector into two parts based on the year. First, we examine the statistics and specifics of merger and acquisition activity in 2023 across various regions and industries. Then, we explore forecasts and expectations for 2024 and beyond.

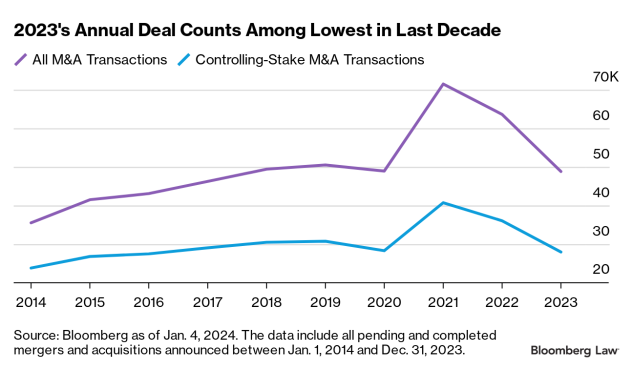

Dealmakers struggled with inflation, geopolitical tensions, rising interest rates, and increased regulatory scrutiny amid economic uncertainty. All these factors depressed M&A activity last year, which resulted in the following:

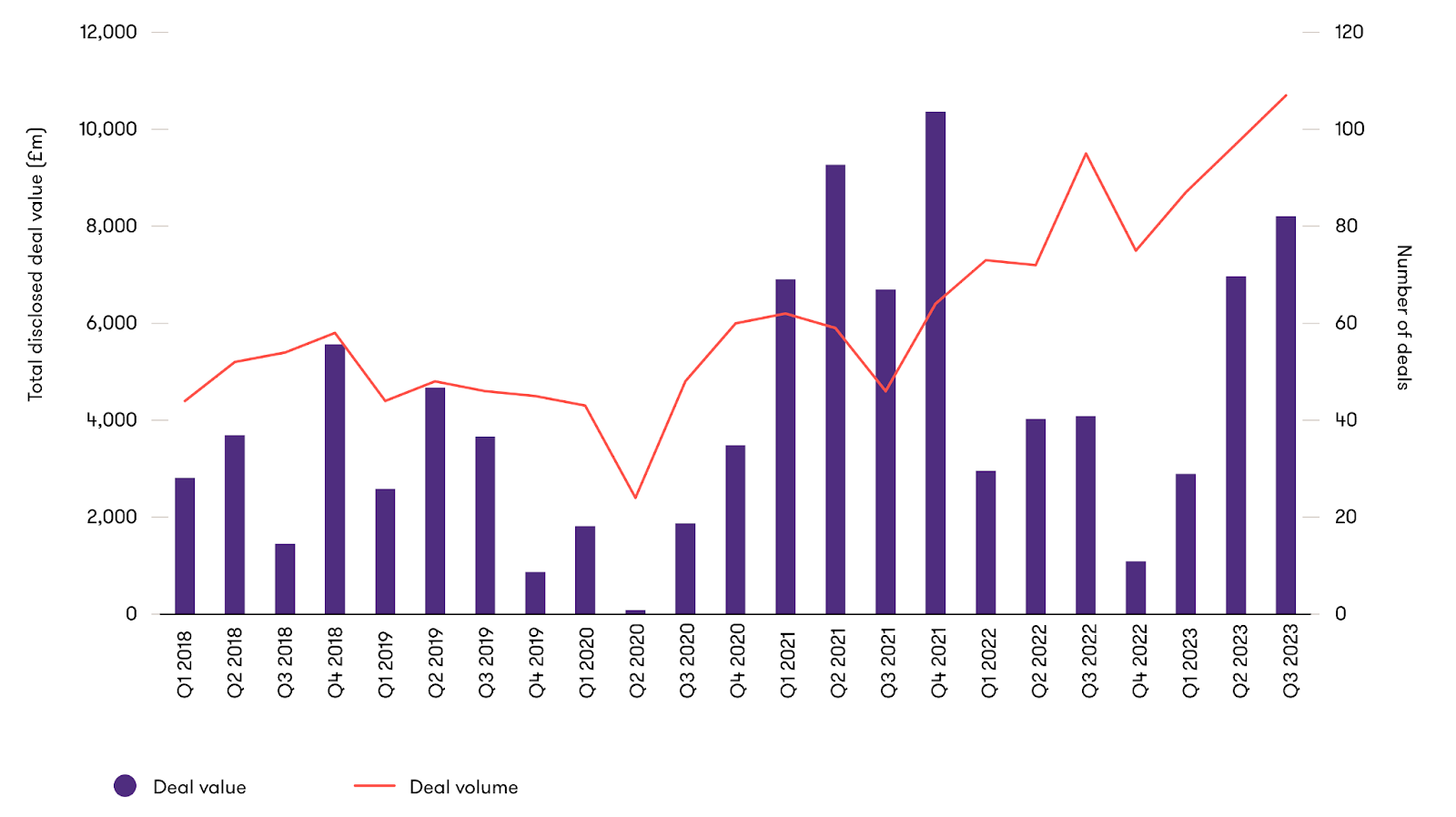

Source: ANALYSIS: Despite Q4 Boost, 2023 M&A Deal Volumes Disappoint

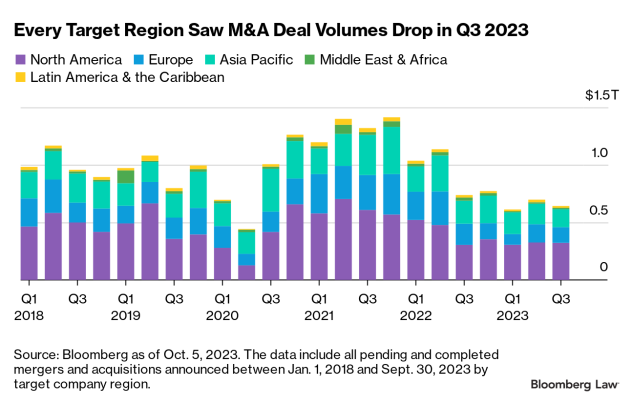

The geography of mergers and acquisitions was as follows:

The region had deals worth $1.46 trillion, a 12% decrease from 2023. However, the second half of the year showed some promising activity. For example, several big deals were announced in September and October, including those between Cisco and Splunk, Exxon and Pioneer, and Chevron and Hess. Also, Arm’s $5 billion debut on the Nasdaq in September was the largest IPO since 2021 and boosted the U.S. capital markets.

Deals totalled $708.2 billion, showing a 26% decline compared to the previous year. Cross-border activity between China and the U.S. remained sluggish. However, Japan experienced a positive trend with a 34% deal increase compared to 2022. Healthcare M&A in the region reached its highest value level ever. Also, the auto industry saw an 80% increase.

Deal activity in the region decreased by 35% to $676 billion. American companies led the way in inbound acquisitions, with deals worth $89 billion. In the fourth quarter, EMEA deals increased by 13% compared to the third quarter, following the trend of the global M&A market.

Source: ANALYSIS: Dismal Q3 M&A Deal Volumes Dampen End-of-Year Outlook

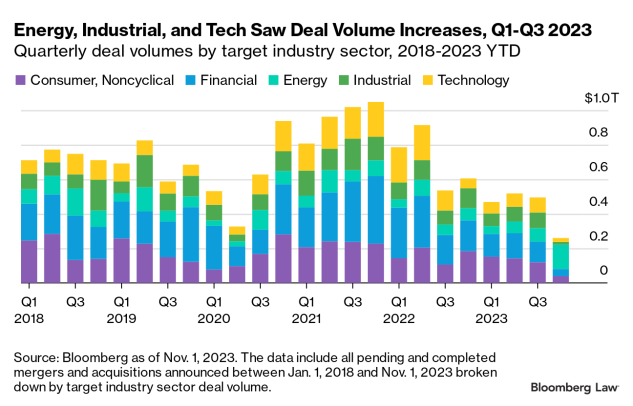

M&A 2023 by industries

The latest insights on industry-specific merger and acquisition activities from PwC and Morrison Foerster are as follows:

Next, discover insights from experts on this year’s M&A climate to better understand the opportunities and challenges ahead.

With elevated borrowing costs, global political instability, and a packed schedule of elections worldwide, 2024 may present a considerable degree of uncertainty. Nevertheless, Morgan Stanley has predicted five trends that will shape the market this year.

Since we offer a brief overview, you may need to check the source for more details.

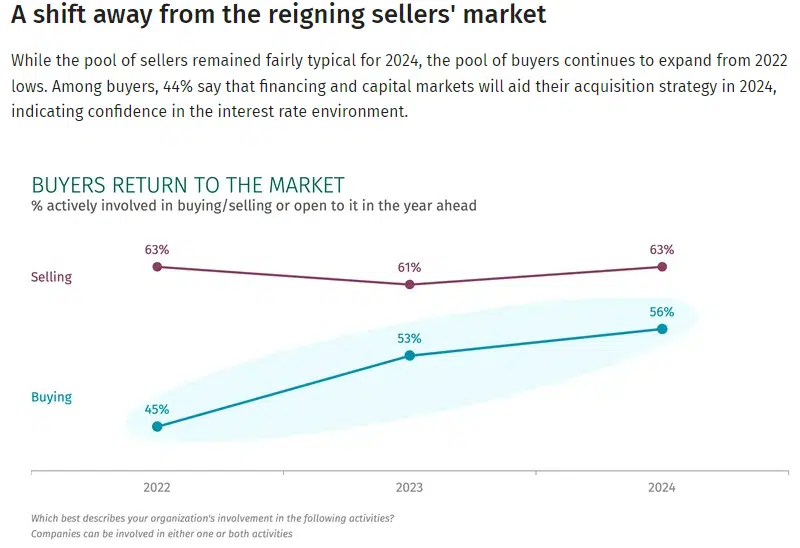

M&A activity may rise in 2024 due to strong corporate balance sheets, improved financing markets, and high CEO confidence, driven by expected revenue and profitability growth.

Financial sponsors may expect increased buying and selling in 2024 due to the large amount of dry powder needed to be deployed and the growing inventory of aging private equity-owned assets that need monetization.

Source: Is Now the Best Time To Sell Or Buy A Business in 2024?

In 2023, the stock market witnessed a notable difference between companies with strong operating performance and those that struggled. It has led to a favourable environment for activist investors to push for changes at undervalued companies, including making certain public companies return to private ownership.

Despite market instability last year, companies continued to streamline their businesses or raise capital by separating and spinning off parts of their organization. This trend is expected to continue in 2024.

European economies have been performing worse than the U.S. economy due to their proximity to the Russia-Ukraine and Israel-Hamas conflicts. It has made European companies more interested in expanding their presence in U.S. markets, which may be a trend for a long time.

Apart from trends, dealmakers can increase deal success by studying recent mergers and acquisitions, including their outcomes and specifics. Therefore, now we invite you to explore the most prominent ones.

For your convenience, we’ve broken down the hottest deals by industry. Thus, you can only study your peers’ experiences and also get more insights from other fields.

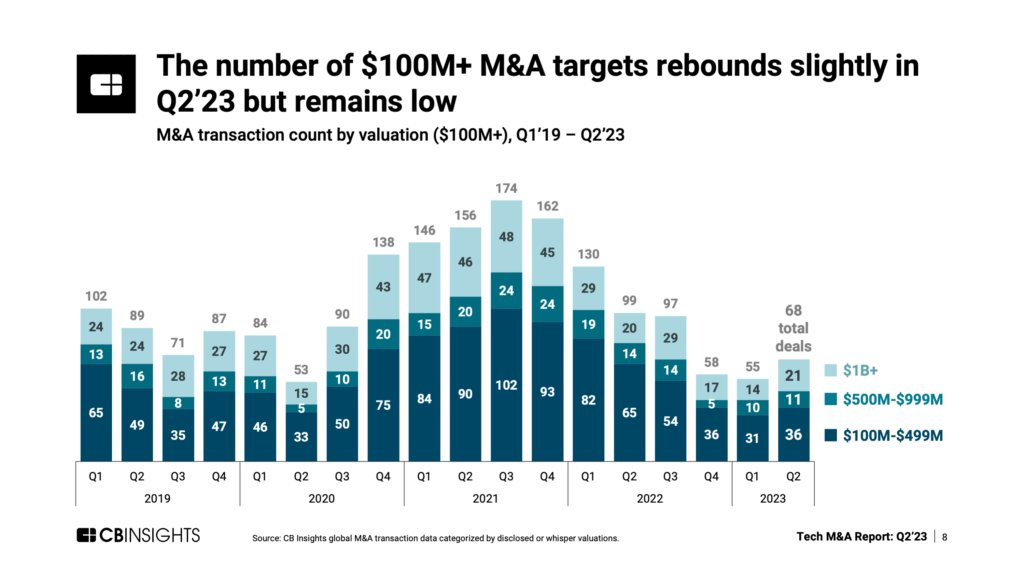

Source: Massive tech M&A deals are ticking up but remain subdued – CB Insights Research

Value: $69 billion

Broadcom closed its acquisition of VMware after a long 18-month deal-making process and reorganized the company into four divisions. Also, more than 2,100 jobs were eliminated, causing customer and partner concerns. The acquisition also faced regulatory hurdles but eventually obtained all necessary approvals.

Value: $28 billion

Cisco Systems has agreed to acquire Splunk in an all-cash deal, expected to close in Q3 2024. The acquisition should enable both companies to deliver excellent customer outcomes and transform the industry by driving the next generation of AI-enabled security and observability.

Value: $12.5 billion

Silver Lake and its co-investors have bought 100% of Qualtrics’ outstanding shares, which includes all of SAP’s ownership interest. As a result, Qualtrics’ stockholders, including SAP, will receive $18.15 in cash for each share of common stock they own. Qualtrics’ common stock is no longer trading on the NASDAQ stock exchange.

Value: $5.8 billion

The deal has created a software powerhouse with an extensive information management and IT security product portfolio. OpenText, which has been expanding aggressively through acquisitions, plans to balance the combined company by reducing its workforce by 8%, resulting in cost synergies of $400 million.

Value: $4.6 billion

Since IBM acquired Apptio, a software provider for managing IT finances and operations, the deal expands IBM’s offerings in IT management and hybrid cloud services. Furthermore, it adds to the capabilities of IBM’s Red Hat and Watson product lines. Finally, the acquisition provides Big Blue with $450 billion of anonymized IT spending data, providing new insights for clients and partners.

Source: Healthcare M&A review Q3 2023 | Grant Thornton

Value: $43 billion

The deal gave Pfizer access to four commercial cancer products, including Padcev, Adcetris, Tivdak, and Tukysa. Pfizer’s oncology portfolio lacked exciting assets to follow up behind Xtandi and Ibrance. With the acquisition, Pfizer is diversifying at a critical time and could accelerate the expansion of Seagen’s portfolio.

Value: $18 billion

Johnson & Johnson has acquired Abiomed, a leading heart, lung, and kidney support technology provider. Abiomed will continue to operate as a standalone business within J&J’s MedTech segment. This M&A will help Abiomed expand its market and financial capabilities with the support of J&J. Meanwhile, J&J will benefit by gaining cardiovascular expertise and focusing on heart failure and recovery solutions. The deal caused the stock price of Johnson & Johnson to rise by 8%.

Value: $14 billion

Bristol Myers Squibb acquired Karuna Therapeutics and accessed a potentially groundbreaking schizophrenia treatment called KarTX. The drug takes a different approach than traditional methods and has fewer side effects. KarTX is up for FDA approval for schizophrenia in September and has the potential for use in other indications such as Alzheimer’s disease psychosis, bipolar disorder, and Alzheimer’s disease agitation.

Value: $8 billion

Signify Health uses home-based visits to identify patients’ clinical and social needs. They then connect patients to follow-up care and community-based resources for a more connected and effective experience. By joining forces with CVS Health, the corporation can take advantage of CVS Health’s collection of assets to connect patients to care more efficiently. CVS Health, in turn, will benefit from this deal by advancing its healthcare services strategy and providing a platform to accelerate growth in value-based care.

Value: $6 billion

LHC Group has 30,000 employees and provides more than 12 million in-home services. With this acquisition, UnitedHealth’s Optum subsidiary will incorporate LHC into its Optum Health, one of the largest employers of physicians in the US. Due to the deal, LHC will provide an expanded network of skilled physicians, while Optum Health will offer a larger network of patients for LHC Group.

Source: ANALYSIS: These Target Industries Show Promise for M&A in 2024

Value: $59.5 billion

This M&A deal will help ExxonMobil solidify its position as the leading player in the U.S. fracking industry and provide it with more drilling sites than any of its competitors. As part of the deal, Exxon will also assist Pioneer in achieving its net-zero Permian goal by 2035. This acquisition presents an opportunity for both companies to collaborate and contribute to the growth of the energy industry in the U.S.

Value: $26 billion

Diamondback Energy is set to acquire Endeavor Energy Partners in a cash-and-stock deal. This M&A will make the combined company the third-largest oil and gas producer in the Permian Basin. The acquisition is part of a recent wave of consolidation in the area aimed at increasing production. It is expected to close in the fourth quarter of 2024.

Value: $11 billion

Chord Energy to buy Enerplus, creating an E&P company focused on the Williston basin. The combined company will have 1.3 million acres and produce 287,000 barrels of oil equivalent per day. Enerplus shareholders will get 0.10125 Chord common stock shares and $1.84 cash for each Enerplus share.

Value: $6 billion

Spanish energy company Iberdola recently sold 55% of its Mexican business to Mexican Infrastructure Partners). While the portfolio included some wind assets, it mainly comprised natural gas assets. In contrast to the European energy sector, which is quickly transitioning to renewable energy, the North American industry still relies heavily on non-renewable sources. This deal, along with Exxon’s deal for Pioneer, illustrates this difference. As of January 2024, Iberdola’s shares have only seen a slight increase compared to when the deal was announced.

Value: $2 billion

Shell Petroleum NV, a subsidiary of Shell plc, has acquired Nature Energy Biogas A/S. This acquisition will give Shell the biggest renewable natural gas producer in Europe. The purchase includes operating plants, feedstock supply, and infrastructure. Shell will benefit from Nature Energy’s expertise in RNG plant technology. Furthermore, this acquisition aligns with Shell’s goal to expand its low-carbon products and services globally.

Whether these are recent M&A deals in 2023 or those concluded earlier, they all reflect a dynamic market driven by economic conditions, industry trends, and geopolitical influences. Therefore, it is essential to invest time and effort in learning from others’ experiences before starting your own M&A venture.